The third global oil price collapse in 13 years has put the oil and gas industry on the back foot. But the energy industry has recovered before – by restructuring and taking advantage of new opportunities.

We take a closer look at what the energy market may look like in the post-Covid-19 era.

Covid-19 Drives down World-Wide Demand for Hydrocarbons

Boom and bust cycles have bedeviled the oil and gas industry since the beginning.

Seasoned workers who’ve experienced downturns before know the drill (pardon the pun) – it’s a time for belt-tightening, cost-cutting, restructuring, and industry consolidation – until the good times come back again.

But this time may be different.

Unlike the most recent oil price crash in 2014 – 2016, the Covid-19 pandemic has led to a precipitous drop in demand for hydrocarbon products that rivals the Great Depression of the 1930s.

Demand from nearly every sector that uses oil and gas is down.

Automotive Transportation Demand

- The economic shutdowns in the second and third quarters of this year drove down gasoline usage dramatically, as workers stayed at home and avoided commuting trips.

Airline Transportation Demand

- Airlines have been operating on skeleton schedules during much of the pandemic as demand for air travel fell off a cliff. Travel restrictions to Canada, Europe, New Zealand, and Australia have compounded the drop in demand.

Electric Generation Demand

- On many days during 2020, wind and solar generation have overtaken conventional fossil fuel electricity production. Working from home has balanced out consumer demand, but slowdowns in industrial production during the height of the pandemic shutdown have curtailed energy demand.

Petrochemical Demand (plastics, fertilizers, fabrics, construction materials, etc.)

- Demand for petrochemicals (including plastics, fertilizers, fabrics, construction materials, etc.) is down due to reduced industrial activity during the height of the economic shutdown, but compared to other sectors is showing signs of recovery.

Economists are downbeat on the prospect of a quick recovery.

For example, analysts at the World Economic Forum don’t expect demand for petroleum products to rebound until 2022 (mainly due to the aviation industry slump), while other consultants worry that 2019 may have been the peak year of oil demand for the foreseeable future.

OPEC Price War Amplifies Impact on US Oil and Gas Industry

Things were oh so different just a few years ago.

The US had finally achieved the unthinkable; we had achieved energy independence for the first time in over 50 years (thanks to growing oil and gas production from so-called unconventionals, e.g. fracking etc.). American energy companies were even beginning to increase export oil and gas to foreign markets.

But, as oil prices dip below $40, the economics of fracking become less tenable.

And this is something that rival OPEC+ oil and gas producers in Saudi Arabia and Russia know far too well.

Rather than limiting production to support oil price levels, foreign producers are continuing to work at production levels that are targeting the economic viability of US oil and gas production companies.

The results are quite sobering.

To illustrate how much the production in the oil patch has deteriorated, Baker Hughes reports in Rigzone that in 2019 it has 632 drilling units in operation, but only 254 in 2020 – this means drilling operations have dropped off by more than 70%.

In a World of Renewables, Investors are Worried about the Future of Oil and Gas Production

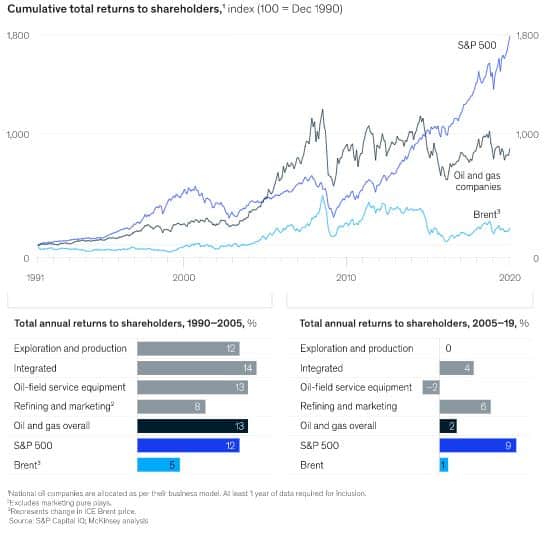

Energy investors are non-plussed.

Even prior to the pandemic, the energy sector was in trouble on Wall Street. After riding high for many years, returns on energy stocks have continued to lag behind other S&P 500 sectors.

And many investors are starting to worry that a significant portion of assets held by major oil companies (e.g. proven reserves in the ground, etc.) could be “stranded” forever, e.g. never be developed. This could become a reality due to one or more factors, including demand for oil has peaked and won’t recover, newer renewable energy sources will make them uneconomic, or government bans on carbon emissions will dramatically curtail their use.

Investors have seen this movie before – with the coal industry – the once-dominant energy source for electricity production (prior to the energy industry’s widespread adoption of oil and gas). New coal-powered power plants and mining operations have been sidelined because it’s become very difficult to attract investors to finance new coal ventures.

Many investors are sensing that the same fate may await investments in oil and gas.

It may already be happening. The energy consulting firm Wood MacKenzie calculates that the oil energy sector has lost $1.6 trillion dollars in value this year alone.

Independent analyst Jonathon Stewart provides his insight on why the market valuation of Tesla has eclipsed that of the five leading US-based oil companies.

A Time for Reinvention Post Covid-19?

Two of the European majors, BP and Royal Dutch Shell, have responded to the Covid-19 pandemic by rolling out plans to reinvent themselves as green energy companies, not just oil and gas companies.

BP has announced new plans to make the company a net-zero-carbon company by 2050 or sooner.

BP tried this once before, of course, with their short-lived “Beyond Petroleum” campaign in the early 2000s (which proved to be more of a marketing campaign than a real change in direction). But they are determined to convince the market they are serious this time about becoming a renewable energy company.

Underscoring the seriousness of their restructuring efforts, BP recently laid off 15% of its workforce and wrote down $17.5 billion in assets and say they may not ever recover all the fossil fuel reserves they have in the ground. BP also sold off their petrochemical operations to Ineos (for a cool $ 5 billion), a move BP CEO Bernard Looney said was necessary for the company to “compete and succeed through the energy transition.”

Like BP, Shell has made tentative moves toward renewable energy investments in the past, most notably their acquisition of a pan-European charging station network for electric cars, which now bears the Shell logo.

As part of their new strategy, Shell plans to eliminate the bulk of its Scope 3 emissions by 2050.

The new restructuring plans cut deep. Facing mounting losses, Shell has written off $22 billion of its assets (including its Australian LNG investments) and plans to lay off 9,000 workers.

Of course, major oil companies always grab the top headlines, but other European companies are looking for ways to restructure as well.

One example is Rotterdam-based Vitol Group, one of the world’s largest oil trading companies, that is leveraging its trading expertise to expanding into used car sales through its new Vava Cars venture.

European Governments and European Union Policy Put the Thumb on the Scale for Green Energy

Why are European oil and gas companies changing their strategy more rapidly than their US counterparts?

The answer to a great degree is they have to.

Concern about the impact of fossil fuels on climate change has been a political issue in Europe for years:

- In 2013, the Germans launched their Energiewende program to transition to clean energy sources.

- In 2015, the German car industry was rocked by the Dieselgate emissions cheating scandal, which spurred Volkswagen and others to pull production on diesel cars in favor of electric vehicles (EVs), as well as government mandates to switch to EVs as soon as 2030.

- In 2016, European countries signed onto the Paris Agreement under the United Nations Framework Convention on Climate Change.

- In 2019, the European Union announced its European Green Deal, which sets a goal of making the continent carbon neutral by 2050, and plans offer significant incentives to help the industry cope with the transition.

And just this week, the UK Prime Minister Boris Johnson announced a new plan to power 100% of UK households with green wind energy by 2030.

The US Oil and Gas Industry is Banking on a Recovery

Here in the US, all energy industry eyes are focused on the prospect of an economic recovery to restore demand for oil and gas products.

At least that appears to be the consensus view of economists at the major consulting firms who have weighed in with strategies on how the oil and gas industry can reduce cash-flow burn until a recovery is underway.

Here is a sampling of the thinking from major brand name consulting and economic forecasting teams:

- Accenture

- Arthur D Little

- Baker McKenzie

- Cushman Wakefield

- Deloitte

- LEK Consulting

- McKenzie and Company

- Platts

- Wood Mackenzie

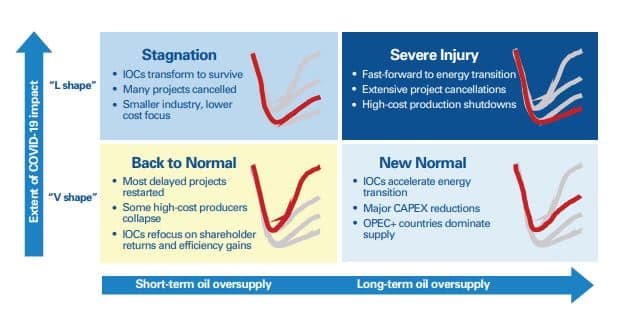

The consensus thinking is that much depends on how a future US economic recovery unfolds – one that can drive increased demand for oil and gas products.

A recovery is expected. But what we don’t know is when and what shape the eventual economic recovery will take.

Will it be a V-shaped recovery curve (quickly restoring us to the pre-Covid state), a K-shaped recovery (which benefits higher-income earners first), or a dreaded L-shaped curve (indicative of a very slow return to “normal” economic demand).

Like their European-based competitors, the American major’s Chevron and Exxon-Mobile have taken a beating during the Coronavirus pandemic.

Yet, unlike BP or Shell, neither has yet to announce a major strategic shift.

In particular, Exxon-Mobile seems to be standing firm in its strategy to be a significant gas and petroleum producer – over the long haul. The company points to economic reports that, despite increased uptake of renewable energy sources, the demand for oil and gas is forecasted to remain viable for the next 40 years – and they intend to continue to pursue that market.

But where does that leave smaller companies in the E&P ecosystem in the meantime?

Clearly, while a major like Chevron or Exxon-Mobil has greater financial clout to withstand the Covid pandemic downturn, many of the smaller exploration and production companies do not have the same resources.

Adding to their financial risk are contracts suddenly being cancelled under force majeure (FM) provisions, leaving many of the smaller players in the oil patch (from well-servicing companies and fracking specialists to the small army of oil and gas landman) looking for a financial lifeline to survive.

Economists estimate that shutting down just one rig can lead to the loss of as many as 300 or more jobs. Not only are the livelihoods of individuals and families at risk, but local government budgets are also on the chopping block as well.

America faces a stark choice. If we can’t assist now, we’ll not only face ongoing economic hardship across the oil patch, but we’ll also lose the energy independence that we’ve worked so hard to achieve since the OPEC oil crisis of 1973.

Formaspace Can Help You Meet Your Goals in a Changing World

When you want to make a change for the better, Formaspace can help.

Our efficiency experts can help provide you with years of experience in making manufacturing, oil and gas operations, and laboratory facilities more productive and efficient.

If you can imagine it, we can build it, here at our factory headquarters in Austin, Texas.

Talk to your Formaspace Design Consultant today and find out why industry leaders, including SpaceX, Oculus, Toyota, Apple, Dell, Google, and Capital One trust Formaspace.