VC money is pouring in to fund the new fintech (financial technology) startups.

According to Forbes, a record $91.5 billion was invested in new fintech startups in 2021 alone – doubling the amount of investment from the previous year.

Across the world, there are now more than 18 fintech unicorns (defined as companies valued at more than $1 billion).

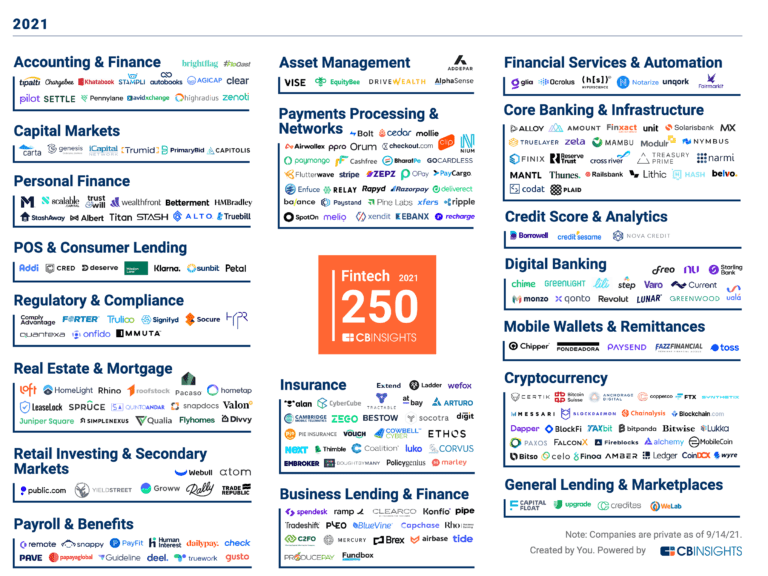

(TIP: CB Insights maintains a list of the 250 top fintech ventures and has produced a handy graphic mapping out their different slices of the market.)

The Race to Turn Your Wallet into a Software Platform

As these fintech startups seek to disrupt the financial services market, we only have to look to companies such as Mint, Robinhood, and Stripe to see how it has transformed the market for managing our personal accounts, investing in the stock market, or paying at the checkout.

It’s truly a race to gain the first-mover advantage and become the market leader in transforming our wallets into a lucrative software platform.

Using Fintech to Improve the Bottom Line for Non-Finance B2B and B2C Companies

But with the majority of VC investment directed at revolutionizing (or displacing) legacy financial institutions, where does that leave non-finance industry B2B and B2C companies?

This question takes on more urgency in the era of Covid, which has brought us unprecedented supply chain uncertainties and the rising specter of inflation.

It’s important to separate the wheat from the chaff.

Don’t get caught up in FOMO (fear of missing out) cause you believe the hype of some of these technologies.

On the other hand, many of these new technologies do offer B2B and B2C companies new, more efficient (and hopefully cheaper) ways to handle payments, get capital financing at lower rates, underwrite insurance at less cost, maintain regulatory compliance with less complexity, monitor fraudulent activity automatically, and more.

Let’s look at each of these opportunities one by one.

Electronic Payment Flexibility

The Promise:

Electronic payments are the bread and butter of the fintech world, tracing its routes back to the introduction of PayPal (and Bitcoin, some would argue). These systems promise faster transfers, at less cost, than traditional bank services and are often available via smartphone access.

· B2B Virtual Payments

In a world of rising inflation, getting paid quickly is important. Electronic fund transfer systems obviate the need for paper checks and speed up funds transfer.

· Embedded Payment Systems

B2C companies (especially SMEs) implementing online checkout systems are increasingly outsourcing these functions to fintech companies such as Stripe, which integrates payment systems with smartphone apps and CRM functions.

· Non-Card Payments

Other fintech startups such as Affirm seek to address the needs of unbanked consumers who want to purchase products online but lack a credit or debit card.

The Bottom Line: From a B2B or B2C business perspective, these fintech companies can simplify e-commerce payments, potentially offering lower commissions, facilitating overseas payments with better FX rates. But when choosing a vendor, you still need to perform due diligence on how these vendors handle chargebacks, protect customer and sales data, help avoid fraud, and how they integrate with your internal controls to avoid mistakenly paying the wrong party – a much bigger risk when transfers can be accomplished in an instant at the touch of a button.

Consumer Finance and Customer Loyalty

The Promise:

Many B2C companies over the years have offered in-house financing services (GMAC anyone?) for large purchases or have accepted credit cards for payment. Fintech startups are offering updated versions of these tools to help companies get money faster (important in inflationary period) while helping increase the purchasing power of consumers (which helps increase sales volume).

· Installment Payments

The Swedish fintech unicorn Klarna is one of several companies championing consumer-oriented installment payment systems that allow consumers (especially younger ones who may not have credit cards) to pay for purchases in installments.

· White Label Credit Cards and Rewards Programs

Credit cards, customer rewards programs are not a new idea, but fintech is pushing the idea of banking platform services (also known as BaaS, or Banking as a Service). These turnkey backend tools and APIs allow non-finance companies to offer company-branded (white label) credit cards or customer rewards programs (similar to airline frequent flier miles).

The Bottom Line:

While these white label credit cards and rewards programs are not new, fintech innovators have driven down the cost and complexity of implementing and managing them, making it possible for even SMEs to offer credit cards and reward systems. Due diligence is called for, however, to make sure customer data remains safe and that the risks (such as fraud or chargebacks) fall primarily on the fintech company side.

Cryptocurrency

The Promise:

We’ve written about the opportunities and challenges afforded by cryptocurrency; click here to read our in-depth report. In a nutshell, the original idea was not unlike PayPal, to create a low-cost, international payment system with a tech rebel/power-to-the-people twist to avoid government interference and regulation.

· Existing Coin Types and Exchanges

The original Bitcoin has come under fire for its massive electric use for mining new coins; giving a lift to competitors such as Etherium, which are investigating new ways to produce coins, as well as multiple ledgers to allow for increased scalability. Tethered coins are another innovation touted as a less speculative alternative, as they are purportedly backed by hard currency (although critics question if this is always true). Finally, there are the so-called hype or meme coins, such as Doge Coins, that have rocked up in value based on tweets from high-profile individuals, such as Elon Musk.

· Future Digital Currencies

Where do national banks stand on cyber currencies? We may soon find out as rumors swirl around the idea of a Chinese E-Yuan digital currency. Not to be outmatched, the Bank of England is also investigating a future digital Sterling currency.

The Bottom Line:

From the perspective of a non-finance company, it’s hard not to view much of the hype surrounding cryptocurrencies as a mere publicity stunt by the likes of Elon Musk and Tesla or the country of El Salvador. Much of the speculation seems to be driven by FOMO – the Fear of Missing Out. Even though some investors have made spectacular returns on these highly speculative coins, others have lost everything due to credential theft and exchange failures. There is also potential for blowback due to the pollution aspect of mining Bitcoins, as well as unknown tax consequences for holding cryptocurrency as countries around the world look to regulate (and tax) the “paper profits” of electronic currency accounts.

Blockchain

The Promise:

For many years, the underlying technology created for Bitcoin has been eyed as a solution to supply chain management’s issues with tracking products, either to ascertain if products were genuine or to track individual items in accordance with regulatory requirements, such pharmaceuticals or food items which might be subject to future recalls.

· Blockchain Technology

Roughly speaking, the original blockchain concept is a shared public ledger that offers the possibility of authenticating if current and past transactions are genuine – without trading partners having to reveal too much financial information. Supply chain specialists have sought to adapt this concept to tracking individual product SKUs (or even individual packages).

The Bottom Line:

Given the incredibly disruptive supply chain logistics challenges that have arisen during the Covid/Post-Covid era, the idea of using blockchains to monitor and fine-tune supply chains frankly seems like a quaint idea more suited to an earlier era of highly stable, just-in-time supply chains. Today’s environment is quite different, with many companies struggling to find “any” available supplier or shipper who can deliver much-needed supplies. Thus the jury is out on whether blockchains will rise to these new challenges.

Non-Traditional Lenders/Fundraising Sources

The Promise:

Just as many fintech startups are seeking to bypass traditional banks and offer new financing tools to consumers, so too are other fintech companies seeking to revolutionize the world of corporate finance and fundraising by offering faster service, lower rates, and funding to companies that might not have blue-chip credit ratings.

· Digital Banks

The so-called Digital Banks of the fintech era eschew traditional brick-and-mortar physical branches in favor of fully automated online interfaces. In many cases, these startups claim to use new scoring methods (rather than traditional credit scores) to extend credit to consumers or businesses.

· SPACs

Special purpose acquisition companies (SPACs) have caught on like wildfire in recent years, updating the old reverse acquisition strategy as a back door to going public. While not technically a fintech innovation, many companies are taking advantage of a large amount of capital floating around, seeking places to invest.

· Peer-to-Peer Lending and Crowd-Funding

Many states have loosened financial banking requirements to facilitate lending clubs or peer-to-peer lending as a lower-cost alternative to traditional bank loans. Crowdfunding tools have also emerged as an important funding source for startups pursuing a new product concept. Fintech has helped accelerate this trend by automating investments, applicant approvals, fund dispersals, and payback management.

· M&A

For companies seeking to grow through acquisitions or seeking an exit strategy to cash out on their investments, new fintech startups are seeking to help with the merger and acquisition (M&A) process by providing automation tools for generating value estimations and performing due diligence.

The Bottom Line:

Many non-traditional/unconventional funding mechanisms, many of which existed previously, have been updated and automated by fintech tools, offering additional funding resources for B2B and B2C companies. These new options might offer greater funding options at lower cost, but as always, due diligence research is critical to success.

Finance Management, Tax Planning, Compliance, Insurance Underwriting, and Fraud/Risk Reduction

The Promise:

While much of the focus of fintech has been directed toward disrupting financial services companies, we are also seeing major innovations in corporate finance management and compliance tools, as well as insurance underwriting and fraud detection tools – with integrated features that go far beyond first-generation accounting and ERP tools.

· Integrated Financial Management

One of the unsung heroes of the fintech revolution is the introduction of next-generation financial management tools, such as Oracle’s NetSuite, which offer ERP-class tools in the cloud, enabling smaller B2B and B2C companies to implement fully integrated systems to monitor and control all their expenses, from inventory purchases to payroll costs.

· Tax Planning and Automated Compliance

Effective tax planning has always been a challenge, even more so as even smaller companies expand their operations overseas. Some fintech startups are seeking to develop AI-based tools to assist in tax planning as well as automating compliance reporting requirements.

· Insurance Underwriting

Fintech startups are not only creating innovations in digital banking, they are also eyeing new ways to modernize the insurance underwriting industry using new information technology methods (including AI-powered tools) to manage risk and calculate premiums, as well as automating policy and claims processes.

· Fraud/Risk Reduction

As more and more financial transactions move online, so too do instances of fraud and other financial risks increase. Fintech companies are developing new automated tools (again many based on AI-powered algorithms) to identify suspect transactions or cyber intrusions that could compromise company accounts.

The Bottom Line:

In an era of disrupted supply chains and rising inflation, companies need to watch their expenditures and protect their assets from fraud. New innovating fintech companies offer the promise of providing innovative, automated systems to assist, but as always, caution is the watchword before implementing a new system – to identify systems that provide real, reliable benefits and avoid “vaporware” vendors making claims they can’t deliver.

What Do Businesses Need Right Now? New Tools to Navigate Economic Disruption and Rising Inflation

The Promise:

If we were to create a fintech wish list to meet the challenges of the current Covid economic environment, what would be at the top of our list?

For most companies, the answer is tools to navigate the economic disruption brought about by supply chain disruptions, particularly interruptions in shipping logistics, as well as maintaining cost controls in light of increasing inflation pressures affecting raw material and labor costs.

· Managing Inventory Capital Carrying Costs

As we’ve written about before, many manufacturing companies are finding it’s more difficult than ever to rely on lean, just-in-time inventory deliveries, which helped keep on-hand inventory capital carrying costs low for decades. But in today’s environment, businesses are scrambling to find new suppliers – so they would welcome fintech systems that could assist in bringing new suppliers on board quickly while keeping track of changing profit margins.

· Distribution Logistics Management

Getting deliveries to their final destination while keeping shipping costs under control is another key concern for businesses that have emerged during the Covid pandemic. Fintech companies also have a unique opportunity to add value here by providing real-time tools to find alternative shippers to meet delivery deadlines while controlling costs to the greatest extent possible.

· Hedging Against Inflation

Fintech companies may also begin to craft new offerings to address the needs of smaller businesses, such as hedging against price increases in raw materials or energy costs.

The Bottom Line:

We will likely see savvy fintech companies pivot their business models and update their marketing messages to address these pressing issues.

Formaspace is your Partner for Ergonomic Workplace Solutions

If you can imagine it, we can build it.

Find out why leading tech companies, including Apple, Capital One fintech labs, Dell, Google, and Twitter, choose Formaspace furniture and space planning solutions for their workplaces.

Take the next step. Speak with your Formaspace Design Consultant today.

{kind=link}